The incentives are split between individuals and businesses with different criteria for each.

FOR INDIVIDUALS

The incentive is given in the form of a rebate and is only applicable for the 2024 financial year. This means only installations between 1 March 2023 and 29 February 2024 will qualify.

The rebate given is 25% against the personal income tax, with a maximum rebate of R15 000 per individual.

The rebate is only given against the cost of the solar panels and not for inverters, batteries and generators.

There will be no recoupment of the rebate if the property is sold, but if panels are sold within 1 year of installation, SARS can claim back a portion of the rebate from the taxpayer.

In order to claim this rebate, the following criteria needs to be met:

- The minimum capacity of a single solar panel installed, must be 275W and can only be claimed on NEW and UNUSED solar panels which is brought into use between 1 March 2023 and 29 February 2024

- The residence must mainly be used for individual domestic Mainly means that 50% and more of the residence is used for domestic purposes.

- A Valid COC certificate for the Electrical installation must be issued and will have to be submitted to SARS when the rebate is

- The VAT Invoice (only VAT registered suppliers to be used) must show the cost of the solar panels separately and will also have to be submitted to SARS when the rebate is

- The individual claiming the rebate, must have a proof of payment, made by him/herself. An individual cannot claim the rebate if he/she did not pay for the installation. This documentary proof will also have to be submitted to SARS when the rebate is

Keep all the documentary proof, as required by SARS, as this will be requested when claiming this rebate. We include the following example to understand this rebate better.

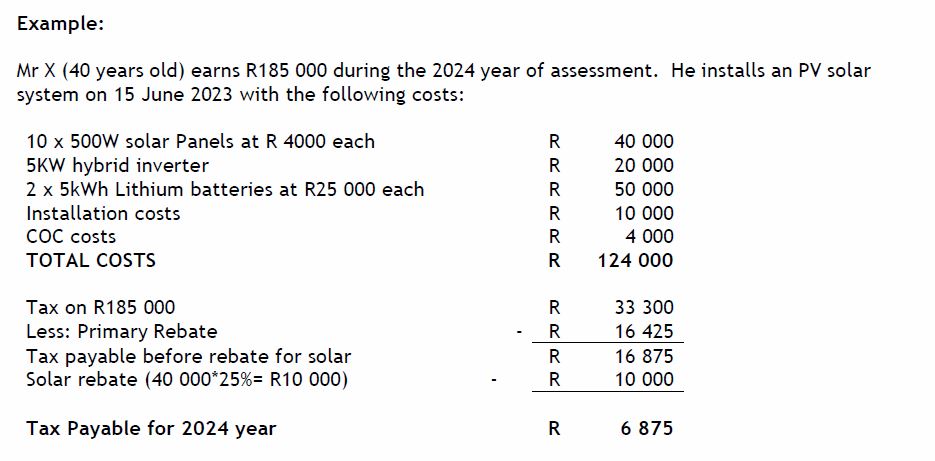

Example:

Mr X (40 years old) earns R185 000 during the 2024 year of assessment. He installs an PV solar system on 15 June 2023 with the following costs:

FOR BUSINESSES

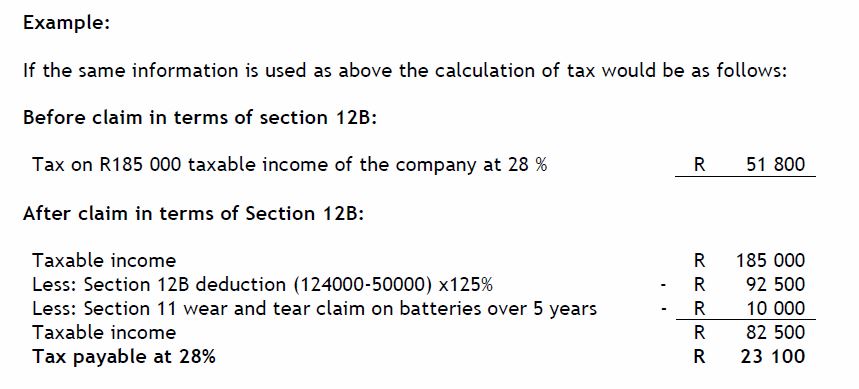

This incentive is not new as it is an existing deduction in terms of section 12B of the Income Tax Act for renewable installations. In order to attract more businesses to install renewable energy solutions, an additional incentive was given to deduct 125% of the cost if installation is done between 1 March 2023 and 28 February 2025. (Normally this would be deducted as 50% in year 1, 30% in year 2 and 20% in year 3)

In terms of section 12B any machinery plant, implement that is used to generate electricity can qualify for these deductions. In terms of Binding rules, issued by SARS, batteries are not allowed to be claimed in section 12B, but must be claimed in terms of section 11.

This article is for general information only and must not be used as professional advice. We accept no responsibility for any mistakes, loss or damage as a result of the use of the information herein. Contact our offices for a consultation, if you require specialised advice.

© Sonja Steenkamp Accountants/Rekenmeesters. 15 March 2023.

{kind=link}

{kind=link}

{kind=link}